No Mercy/No Malice

Casper Should Not Go Public

If it does, the stock will shed 30%+ in the first year

In 2015, one of my students asked me to invest in his business. He was sourcing cotton in Egypt, milling it in Israel, and then landing a set of sheet sets, duvets, and pillows in Brooklyn for $79 that he would sell for $129. The value proposition was clear: bedding that sold elsewhere at $400, for a lot less. In what was to become Brooklinen, The Fulops, a husband and wife team, had secured orders online before the cotton was purchased. This is the definition of good marketing and business strategy — finding products for your consumers versus finding consumers for your products (piling stuff high in a store and hoping people buy). Streamlining the supply chain to offer better value on a better product is the way to go.

In 2015, one of my students asked me to invest in his business. He was sourcing cotton in Egypt, milling it in Israel, and then landing a set of sheet sets, duvets, and pillows in Brooklyn for $79 that he would sell for $129. The value proposition was clear: bedding that sold elsewhere at $400, for a lot less. In what was to become Brooklinen, The Fulops, a husband and wife team, had secured orders online before the cotton was purchased. This is the definition of good marketing and business strategy — finding products for your consumers versus finding consumers for your products (piling stuff high in a store and hoping people buy). Streamlining the supply chain to offer better value on a better product is the way to go.

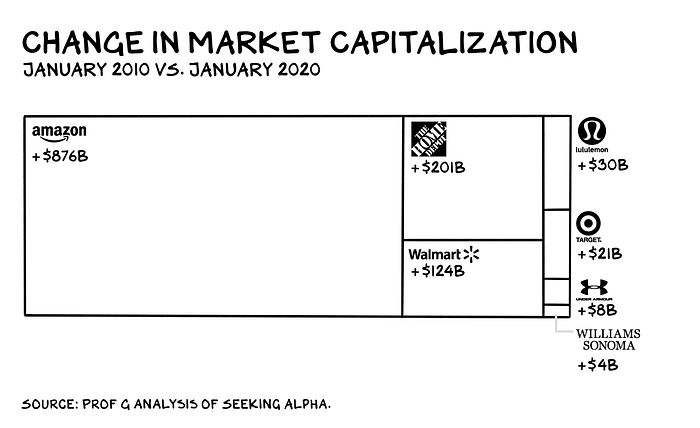

In 1953, Chuck Williams bought the Ralph Morse Hardware Store in Sonoma, California. He gradually converted the merchandise from hardware to French cookware, which was hard to find at the time. Over the last 50 years, Williams-Sonoma built billions in shareholder value zigging versus zagging. The key isn’t selection, but a lack of selection. Williams-Sonoma doesn’t have the most toasters, it has the Dualit New Generation 4-Slice Toaster — the right toaster. Why is it the right toaster? Because Williams-Sonoma merchants have better taste than you—the core value proposition of specialty retail.

The cookware retailer also sells the iconic Williams-Sonoma Classic Solid Apron in Claret Red. Why would you pay $25 for $2 of cloth? Because this apron says you love people (cooking for others is an instinctual form of caregiving … remember Mom?) and that you are successful. A mix of attributes that makes you attractive to other people. Self-expressive benefit and voice are powerful drivers of value.

Restoration Hardware was started 40 years ago after Stephen Gordon had trouble finding high-quality home hardware and fixtures. Since then, the firm has opened enormous galleries and shipped catalogs the size of phone books. Neither of these made any sense until they did. The galleries and phone books have been huge successes and now feel obvious. Breaking the mold in your category (leadership) pays off.

Voice, self-expressive benefit, proprietary product, innovative distribution, and leadership should all add up to margin. Specifically operating margin.

Casper

Casper has filed to go public. Let’s look at how they stack up against traditional players and new kids on the block in DTC/specialty retail.

Casper is a nice brand in a growing market — the sleep economy. Sure, call it that. The alternative, mattress stores, are the stuff of Tarantino movies. You expect a guy with a sawed-off shotgun to roll in and take hostages. The biggest factor in a company’s growth isn’t the company itself but the incompetence of the incumbents. Casper and the 175 other online mattress retailers (think about that) have disrupted the industry with a better DTC experience.

However, Casper will not go public, as it has no business being public. Casper’s numbers are a sign of a frothy economy: firms that should be sold in the private market doing a kabuki dance (“technology” mentioned over 100 times in prospectus), asking people to suspend their disbelief until the founders, VCs, and bankers sell their shares and get their fees. That’s not going to happen. Here too, yogababble won’t cut it: “We believe we are the first company that understands and serves the Sleep Economy in a holistic way.”

The economics work better if Casper sent you a mattress for free, stuffed with $300.

Uber breached the fire door of rational thinking, and in a collective cry of “we won’t be fooled again,” the door was slammed shut on We. Casper won’t even warm the IPO door as sanity sprinklers are extinguishing any consensual hallucination between Casper/Goldman and investors.

Goldman’s core attribute is its reputation as an accelerant for people’s careers. This draws the best and brightest, enabling GS to charge higher fees, pay their people more, and wash, rinse, repeat. In addition, it usually affords them a finer filter for clients and businesses they play with. Goldman is a B2B firm, and moving into consumer banking and credit cards is similar to McKinsey launching a line of suits. Makes sense, sort of. Goldman’s name on the upper left of an S-1 that will be stopped at the border speaks to how desperate the firm is to keep their remaining retail bankers busy, and how strained the IPO business has become.

Casper will not go public. If it does, the stock will shed 30%+ in the first year. Away, a better business with a more differentiated product in a less competitive category, may or may not get out. If I were advising Away, which I am not, I would give them the same counsel I gave to Casper management (talented, impressive young men) 24 months ago: sell. Casper should be acquired by a bigger retailer, like Target, or any middle-aged retailer looking for a shot of Botox. That would give them momentum in the sleep category, domain expertise in DTC, and Casper would get the scale they clearly don’t have. They may have missed their window. Away’s is closing. The gangster here will be Warby Parker, who will have one of the more successful retail IPOs in recent memory.

Casper and Away have to pay to generate traffic while Warby Parker gets nearly 80% of its traffic organically. Warby is the tallest midget of startup retail, as the sector has been a wonderful place to shop and a terrible place to invest or work. Unless, of course, you work for an unregulated monopoly. Monopolies not only prematurely euthanize big firms that are good tax payers and employers but perform infanticide on emerging retailers.

Casper is being drowned and likely won’t survive. Away needs to be adopted by someone who will feed, clothe, and protect them. Warby looks to have the muscle and fat to survive an Amazon winter and emerge stronger.

The financial press argues Amazon and other disruptors have resulted in millennials enjoying subsidized sleep, rides, and desks. CNBC leads us to believe there are startups everywhere. There aren’t. The greatest engine of job growth, small business, is on life support. Half as many firms are founded today as during the Carter administration. Even the most promising struggle to find the scraps ignored by the great white sharks of big tech.

Wages are stagnant, and student debt has never been higher. But mattresses, glasses, and dog walkers have never been more affordable. There’s never been a better time to have the money young people don’t have.

Life is so rich,

Scott

Originally published on profgalloway.com.