The Economics of Asymmetric Information

“If he wants to sell that horse, do I really want to buy it?”. The question represents a problem that’s as old as markets themselves. The problem concerns what’s called “information asymmetry”, and this article explores some of the most profound literature on information asymmetry and economic policy.

Market failure refers to a situation where free markets fail to achieve pareto optimal outcome. Such scenarios manifest particularly when the key assumptions of the free-market economic system fail to satisfy. Among the many assumptions made by the classical economists, “perfect information across all market participants” has been consistently attacked by the academia since the 20th century.

People generally think about imperfect information as cases of exogenous uncertainty; lack of perfect foresight about events that might occur outside the economic system (We did not see the pandemic coming, did we?). Unlike exogenous uncertainty, imperfect information may also be endogenous to the economic system.

Different people might know different things in a market. An insurance buyer might know more about his health condition than the seller; a seller of a product might know more about its quality than its buyer; an employee might know more about their ability than the employer and so on. Such situations are examples of what is called information asymmetry; a special case of imperfect information caused by an imbalance between two negotiating parties in their respective knowledge of relevant factors. As we shall see later on, asymmetric information may produce detrimental effects on the economy’s efficiency, and cause problems that are much expensive to fix.

We begin with the question that gave the problem of asymmetric information such significance in economic literature.

How can the tax system be optimally designed?

As the Marxian dictum goes;

“From those who are able to those who are in need.”,

redistribution essentially means taxing the rich and transferring to the poor. Although an issue that puts us in a fundamental philosophical dilemma (Do we really own ourselves?), redistribution theoretically makes perfect sense from an economic welfare perspective. After all, the Second Fundamental Theorem of Welfare dictates; as long as markets remain competitive, pareto efficiency can be achieved with any redistribution of initial wealth. In other words, it would make no difference at all to the social welfare even if a 100% income tax were imposed on incomes above the median income, and the sum transferred to those earning lesser the median income, as long as markets remain competitive (Here’s a surprise: This works the other way around too; from this perspective, it would also make no difference on welfare if the poor were taxed to subsidize the rich).

But there’s a problem with income redistribution which the welfare argument ignores. Although income tax balances the distribution of income, it distorts the incentives to produce and renders the labor market uncompetitive. For instance, a 100% marginal tax rate above incomes higher than the median would disincentivize the high-income workers to exert any more effort than what is required to earn just the median income. Equity therefore comes at the cost of efficiency, as income taxes not only affect the workers’ after-tax income but also their pre-tax income.

How should the optimum tax policy be designed then? This is a big question; one whose significance is undoubtedly of a titanic scale for the social planner. It was William Vickery who posed the problem of optimal tax policy for the first time in his 1945 paper “Measuring Marginal Utility by Reactions to Risk”. However, its significance was much overlooked until later in the century when James Mirrlees revitalized the issue and gave it much clarity in his 1971 paper “An Exploration in the Theory of Optimum Income Taxation”.

Mirrlees’ approach to the problem focuses on the heterogeneity among the taxpayers that remains unobserved to the social planner. The problem at hand is this; the innate ability to earn income differs across individuals, and their income depends on their respective innate ability and effort. Although the taxpayers can directly observe their respective ability (wage rate(w)) and effort (labor hours (l)), the planner can only observe their income which is essentially the product of the two (w*l). Given this is the case, imposing taxes on high-income earners in an attempt to tax those of high-ability discourages the low-ability taxpayers to exert the effort required to earn higher levels of income.

For example, assuming a relatively higher wage rate for a doctor compared to a janitor, the government might confuse a hard-working janitor to be a lazy doctor. If the janitor is taxed the same amount as the doctor, this would demotivate the janitor to work harder than what is required for them to earn a median level of income. Therefore, the central problem for the planner is to make sure that the tax policy provides sufficient incentive for the high-income tax payers to keep producing their corresponding levels of output irrespective of the high tax burden they must bear.

Although the 1971 essay misses out the word “information asymmetry” entirely, the optimal tax problem is essentially framed as a game of asymmetric information between the social planner and the taxpayers. The planner wants to tax highly-able taxpayers and give transfers to those of low ability and at the same time ensure that the tax policy does not incentivize those of high ability to mask themselves as being of low ability. Vickrey and Mirrlees were jointly awarded the 1996 Nobel Prize in economics “for their fundamental contributions to the economic theory of incentives under asymmetric information”.

Information Asymmetry

Around the same period as Mirrlees, another prominent economist was venturing into something similar. George Akerlof produced his seminal work “The Market for Lemons: Quality Uncertainty and the Market Mechanism” in 1970. Akerlof was more focused on the private market, and he encountered a problem similar to what was posed by Mirrlees in the used car market, insurance market, labor market and so on. Under Akerlof’s framework, the optimum tax problem became just one example of a general phenomenon in which information is unevenly distributed across two negotiating parties, or situations involving information asymmetry. Needless to say, Akerlof won the Nobel Prize in 2001 for his 1970 essay, and we shall briefly discuss some of the main ideas. (Also, Akerlof’s wife was Janet Yellen, the former US secretary of the treasury. Quite a power couple.)

Let’s start with the used cars market by assuming a scenario. Say, there are two types of used cars in the market; bad cars (lemons) and good cars (plums), with q and (1-q) being the share of lemons and plums in the market respectively. Say, the market value of a plum is $2400 and a lemon is $1200. The buyer computes the expected value of an average car as v = q*1200+(1-q) *2400, and is willing to pay no higher than that amount for their purchase. Assume the buyer knows all of the information above except for whether or not the car offered for sale is a lemon or a plum.

As shown in the graph, the buyer’s valuation is inversely proportional to the share of lemons in the market. Because the information of the car’s type is available only to the seller and not to the buyer, it becomes impossible for the buyer to purchase a plum simply because the seller of a plum is unwilling to transact at the buyer’s average valuation. As more and more buyers purchase lemons the share of lemons increase and with it the average valuation goes down further, crowding out the sellers of plums from the market till the market eventually collapses.

Adverse Selection

The case with insurance markets is also the same, except for the fact that in this market buyers have more information than sellers. Take health insurance for example. The insurance company can only acquire probabilistic information about the health of its customers, but cannot identify exactly whether or not an individual is healthy (plums) or unhealthy(lemons). Based on the probabilistic information the company has to price its insurance premium, but the price ends up being too expensive for healthy buyers and affordable only for those who are unhealthy. Such situations where worse risks (lemons) crowd out the good risks (plums) from the market is called adverse selection.

Adverse selection is the reason why evenings are not the best time to go buy apples. If the price for both good and bad apples in a basket are the same, the freshest ones get sold out in the morning, and only the ones no one wants to buy at that price are left in the evening. If the leftover apples fail to get sold by the evening, then that situation is referred to as a market failure; as there was room for increasing the overall welfare in a way that made everyone better off. The market would be considered efficient only if all the apples were sold out.

Let’s get back to insurance. Adverse selection is bad because it disallows the market to operate at the pareto optimal. In our case, although both the insurance seller and the healthy buyer have a room for a transaction that can maximize the welfare for both, it fails to happen because of the adverse selection problem.

The consequences can get disastrous eventually. As the insurance seller cannot make profits because no healthy buyer is purchasing their insurance (just like the tax problem, insurance is basically the redistribution of income from the healthy ones to the sick ones). The seller reacts by increasing the price (or premium) to breakeven, but doing so causes even more healthy buyers to leave the market and thereby increases the seller’s loss further. Therefore, adverse selection leads to a scenario called a death trap, a situation where the insurance seller is eventually only left with unhealthy buyers as a result of increasing the premium to offset its losses.

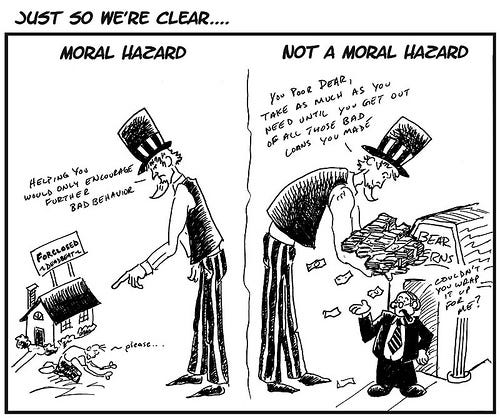

Moral Hazard

Another important consequence of asymmetric information on welfare is what’s referred to as “Moral Hazard”; an inefficient situation that arises when the person making the mess doesn’t need to clean it up.

As the cartoon shows, a great example of moral hazard would be the 2008 mortgage crisis. The government did not subsidize the high debt burden of the borrowers to avoid the possibility that the in the future, borrowers would be incentivized to borrow more than their ability to pay in the future by relying on the safe hands of government who would then bail them out. However, the policy proved to be hypocritical, in the sense that the state bailed out the big banks and did not let them go bankrupt, irrespective of the fact that it was them making highly risky investments that caused the recession in the first place.

Going back to the insurance market, moral hazard happens because of ex-post information asymmetry (or what is referred to as ‘hidden action’ in Mirrlees (1971)) i.e., the insurance seller cannot monitor the behavior of the buyer after the policy is sold. For example, a person might choose to care less about their health because they’ve got an insurance. Similarly, the redistribution problem discussed earlier; that taxes makes workers want to work less, is also essentially a problem of moral hazard.

Moral hazard leads the market to an inefficient outcome because the cost of an insured’s immorality has to be born by the insurer. And this problem as it appears is much difficult to solve because the behavior of any agent is almost impossible to monitor completely.

Bridging the Information Gap: Signaling and Screening

It has been clear by now that information asymmetry causes adverse selection and moral hazard, both of which lead the market towards inefficiency, or even worse, collapse. So how do we go about dealing with information asymmetry?

The answer appears to be pretty simple; by balancing the level of information across the negotiating parties. Let’s first look at the problem with adverse selection by going back to the apples market. How can we make sure all the apples get sold? Simply by separating the good apples from the bad ones in the first place and charging a relatively higher price for good apples.

It’s the same problem in the market for lemons, if there were two different prices for plums and lemons, then the death spiral caused by adverse selection could be avoided and everyone could be made better off. However, a fundamental question remains; how can the buyer know whether or not a car is a lemon of a plum?

There are basically two strategies to get the answer; Signaling and Screening. Going back to our case about the market for lemons, a plum seller can offer guarantee to the buyer to signal that the car being sold is a plum. On the other hand, a buyer can screen a lemons seller by offering them to purchase the car at a relatively higher price only if the seller can offer a guarantee. By either signaling or screening, adverse selection caused by information asymmetry can be avoided.

However, balancing the level of information across the negotiating agents might not always lead to the best outcome. Let’s consider the insurance market for example. Assume there’s a screening technology that accurately predicts if or not someone will get cancer in their life based on their genetic factors, and the insurer has this technology at their disposal. If a buyer goes to the insurer for protection against the risk of getting cancer, and the insurer knows that they’ll get cancer then the insurer will not have the incentive to protect them at any premium amount lower than the costs incurred in treating cancer.

This is the reason why most old people have a hard time getting insurance, even though they’re the ones most vulnerable to health risks and therefore need it the most. Perfect information symmetry in the insurance market is therefore paradoxical.

Avoiding Moral Hazard: Splitting the Burden

Similarly, situations involving moral hazard requires more than just ascertaining the type, but also designing contracts that incentivizes the negotiating agent to act in a manner that leads to an efficient outcome for both. For instance; in the case of the insurance market, it would be favorable for the insurer to institute a co-pay and deductible in the contract, so that the buyers become liable to pay a part of the services they receive.

However, this also isn’t a complete solution in itself as it only partially ensures avoidance of moral hazard (i.e., it can only be fully avoided if there’s no insurance at all).

Conclusion

Asymmetric Information is indeed a problem with significant consequences and no fit-all solution at disposal. The subject has also attracted significant attention from the Nobel community, and many profound economists have been awarded the status of a Nobel Laureate for their contributions in the area. However, it cannot be denied that the subject still provides a fertile ground to make a fundamental contribution. Lots of fundamental questions remain unanswered; How can the insurance market function optimally? How do we ensure agents to act morally? And also possibly, more right questions are yet to be asked.