What Might Bowie Have Done with Crypto?

How the $2 trillion crypto asset class taps into ‘scarcity credibility’

Any firm that approaches $1T in value has tapped into a basic human instinct. Consuming, signaling, loving, and praying have been the fuel of Amazon, Apple, Facebook, and Google’s ascents, respectively. That the crypto asset class universe has reached $2T reveals, I believe, that it taps into two attributes we instinctively pursue: trust and scarcity.

Trust

Our superpower as a species is cooperation, which requires trust. It’s the reason banks, traffic lights, and anesthesiologists exist. Even before crypto, creative minds have been drawn to finance, as trust creates opportunities for leverage and securitization. In 1997, seeking more control over his songwriting catalog, David Bowie raised $55 million with Bowie Bonds. The bonds paid 7.9 percent interest over a 10 year-long term — a scant premium to a U.S. 10 Year Treasury Note at 6.4 percent. What made Bowie Bonds unique was the collateral, or source of trust: future royalties on Bowie’s music, which the bondholder felt people would continue to value. Moody’s rated the bonds A3 and Bowie used the proceeds to buy out his former manager, shoring up the bonds and securing long-term control of his music.

Though innovative in its collateralization, the Bowie Bond was on its face a vanilla financial instrument, no different in form than a bond issued by GM or P&G. In order to connect his art and potential investors, Bowie had to rely on the (expensive) apparatus of traditional gatekeepers in finance and entertainment to imbue his bonds with the essential attributes of trust and scarcity. The royalty stream (trust) was mediated by lawyers and accountants in big publishing houses, and the legitimacy of each individual bond (scarcity) was dependent on the financial powers of Wall Street.

What if Sir David Bowie (note: he declined knighthood in 2003, but it’s my blog) fell to earth in 2021? What might Bowie have done … with crypto?

Scarcity

People like scarcity — a lot. Owning something scarce makes one feel unique, and signals success and worthiness as a potential mate. Scarcity is also an instinctual trigger for obsession — when we sense a scarcity of something, be it food or a mate, we are programmed to become obsessed with finding it. Art auctions, the (pre-pandemic) lines outside Supreme, and the margins on a Panerai Tourbillon prove this point.

A Van Gogh and a Rothko are both unique, and therefore scarce, because they are made of atoms, and it is impossible to arrange a second set of atoms in an identical configuration. Print artists, whose lithographs are made to be reproduced without alteration, use a small “17/100” written in the corner, to distinguish each print and bestow scarcity upon it.

To hold value, scarcity must be credible. The dirty (not-so) secret of the art world is that art buyers, and even professional art appraisers, struggle to discern originals from forgeries. A well-made forgery provides the same practical value as an original — you can hang it on your wall and bask in its profundity. Yet the art world invests millions of dollars in identifying the “real” version of valuable works; once unmasked, forgeries are nearly worthless.

Digital art suffers from perfect reproducibility, and hence, a lack of scarcity. There is no “real” version — even in the artist’s studio, copies proliferate in backups, on shared drives, and in cache files. For decades, we have experimented with watermarks and anti-piracy tech to try and enforce a physical, world-of-atoms scarcity on digital goods. By contrast, non-fungible tokens, (NFTs) reflect a digital-native approach to credible scarcity.

Attaching an NFT to a digital artwork gives the NFT owner discretion to designate any digital copy of that artwork as the sole authentic copy at any point in time. This approach jettisons our world-of-atoms obsession with a specific physical object, and acknowledges that scarcity has always been a function of bits, not atoms. Value is in the eye of the beholder.

Let’s Dance

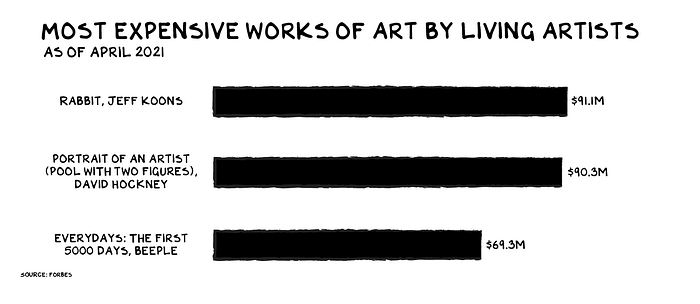

On March 11, digital artist Beeple collected $69.3 million (minus the hefty fee of his gatekeeper, Christie’s) from the auction of an NFT associated with a collage of his 13 year-long project of daily digital artworks. The media has made much of the fact that the buyer of Beeple’s NFT, crypto investor Vignesh Sundaresan, did not obtain any tangible “thing” for his money. The art itself is available for anyone to view — for free — on Beeple’s web site. But collecting art has rarely been about the thing. It’s about credible scarcity.

NFTs create and capture the value of scarcity cred in a massively dispersed fashion that bypasses gatekeepers and taps into capital anywhere. At the high end, digital art sold for millions doesn’t really need an NFT, just as Bowie didn’t need crypto to securitize his royalties in 1997. Christie’s could have just as easily sold an embossed paper certificate, and entered the buyer’s name in a leather bound book securely held at Christie’s headquarters. But that sort of infrastructure isn’t available to the vast majority of digital artists, whereas anyone can create an NFT. Nyan Cat, a pop culture meme, isn’t likely to appear at Christie’s any time soon, but as an NFT it sold for nearly $600,000.

All the Young Dudes

Scarcity cred explains more than NFTs. The entire $2T crypto asset class rests on scarcity cred. Bitcoin’s attractiveness as a store of value is a function of its scarcity cred, as it has a built-in limit of 21 million coins. Compare that to the USD: Almost 30 percent of the U.S. money supply has been created since 2020.

There’s a variety of crypto technologies/products/platforms evolving new means of creating and capturing value in a network: Ethereum, Ledger, Uniswap, Hedera, Cardano — a soup of innovation that is, similar to other tech innovations, not doing anything new … just doing it better.

It remains to be seen if this approach will take hold. Crypto’s energy use is a source of real concern, but the hardware and software are evolving quickly to become far more energy efficient. Even Beeple thinks the current mania is a bubble, as he told my podcasting partner Kara Swisher. But the history of the art market is a history of bubbles, as are the histories of finance and the internet. All are still with us.

Crypto is firing on the walls of the world’s financial citadels. Naturally, the generation of leaders behind those walls is not inclined to acknowledge the Wildlings outside. But scoffing at novel technology, be it a mangonel, black powder, or blockchain, rarely ends well for the legacy asset holders. Bigger castles are already being erected on the hill just above the naysayers … in this case, in mere years vs. generations. It’s likely that on the day of its imminent public listing, Coinbase will be more valuable than Goldman Sachs. A reasonable question in the JPMorgan and Goldman board meetings:

How the fuck did we/you let Coinbase happen?

But that’s another post. Unencumbered by regulation, reticence to destroy legacy assets, or boomer brains that just don’t “get it,” crypto is a $2 trillion disruptive force. I can validate that anybody over 50 has trouble understanding this stuff, and am fairly certain that the number of candles on the CEO’s office party birthday cake is inversely correlated to their understanding of crypto.

Of course, in a system that is still heavily skewed in favor of older, white men, “getting it” for that cohort can be worth billions. Crypto investors Michael Novogratz and Michael Saylor, both over 50, have a combined net worth approaching $10 billion. But they are the exceptions.

Bowie himself was 50 when he issued Bowie Bonds. A prolific art collector, Bowie was also famous for championing young creators, and being enamored of technology: In 1998, he launched his own internet service provider, BowieNet, an interactive music community a decade ahead of its time, and the next year, he launched an online bank (BowieBanc). “If I was 19 again, I’d bypass music and go right to the internet,” he said at the time. In a prescient 1999 interview, he is a time traveler explaining the future to our skeptical past.

RIP Bowie, you would have loved crypto.

Life is so rich,