No Mercy No Malice

Why Peloton Will Win the Biggest Work-From-Home Experiment in History

The fitness company is pedaling its way to over $1 billion in revenue this year

Before SXSW was canceled, I was planning on going despite the coronavirus. While catching coronavirus would be bad, worse would be passing it to someone vulnerable. But I put my trust in the CDC, which said travel is okay and to wash my hands and not to touch my face. Great, there goes that hobby.

Ozzy Osbourne and Facebook both pulled out of SXSW. Pretty sure Ozzy already has it — he used to eat bats on stage. I was scheduled to do a keynote with Katie Couric and Jim Bankoff. This is something I never imagined, and I’m still processing what connective tissue or butterfly flapping its wings in the Amazon almost brought me and Katie together in the Lone Star State.

I used to find comfort in our leadership during times of crisis — both George W. Bush and Barack Obama were steady hands through 9/11 and the Great Recession respectively. But no longer. The initial response from Western leaders was to manufacture and distribute low-cost testing kits. In the U.S., we cut interest rates, and our president proposed to cut funding for the CDC by 9%. We then had someone who botched an HIV outbreak and doesn’t believe in evolution try to explain why the kits aren’t ready. Then he was tasked with walking back the president’s statement that infected people should go to work.

Note: Before sending hate mail, recognize it’s not partisan to observe idiocy. The government has one job: to overreact. Not declare victory when cases are doubling.

Taking precautions can save respiratory systems and, most importantly, the lungs of people with weaker constitutions. Yet I wonder what has been the cost to our nervous systems during the three months of fear and hype we’ve been through in the shadow of screens with increasingly creative and scary infographics. Media algorithms know: fear = engagement. Your lungs are okay, but how’s your resting blood pressure? Stress affects more than your respiratory system, and the effects are long term.

Let’s. Talk. Stocks.

Last week we wrote about playing defense: companies that will experience a temporary downturn but are robust enough to survive the shock — e.g., Hudson News (-47%), American Airlines (-42%), and Carnival (-33%). Their stocks should return to pre-coronavirus levels. CNBC focuses on big companies so it can run ads from trading firms hoping seniors will let their returns be eaten up by fees. There is scant reporting of the sector that, similar to seniors and people with underlying health conditions, will have a much higher fatality rate: small and midsize business. Apple and SXSW will be fine. It’s the regional airline and the event planning firm that may not make it out of the ICU.

This week, we talk offense — companies that will register an increase in business due to Covid-19 and may enjoy a step-change upward. Zoom is one of those companies. Today we focus on Peloton. We are in the midst of the largest work-from-home experiment in history. We are also likely experiencing a shift to working out from home.

T algorithm

Peloton’s rally will outlive the coronavirus. The firm has all the makings of an exceptional business and will clock over $1 billion in revenue this year — year-over-year growth of 69%. In addition, Peloton ticks many of the boxes in the T algorithm. The T algorithm is eight factors that could take a company to a trillion-dollar valuation. (We dive deep on this in my two-week Strategy Sprint course — sign up for the April sprint session here.)

Recurring revenue: Peloton is quickly approaching 1 million connected subscribers who are locked into a recurring revenue relationship with the brand. The firm is also offering an option to pay a monthly fee vs. buy. The connected fitness firm enjoys a Netflix/Prime-like 93% retention rate. This is greater than most SaaS firms.

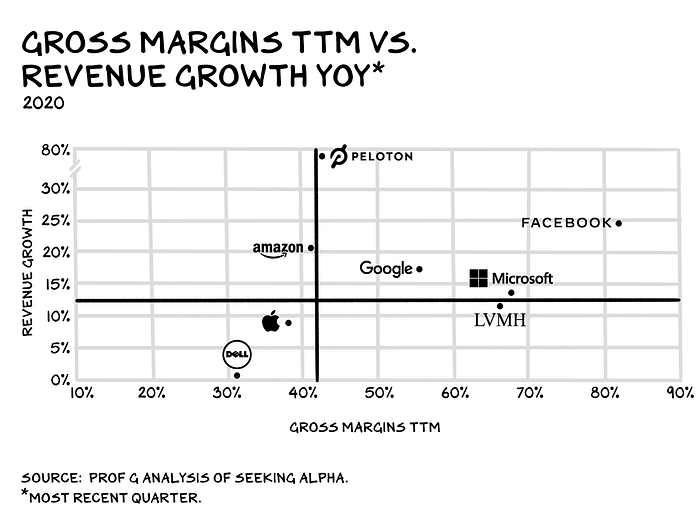

Margins: Margins are the litmus test of the value add, or differentiation, that an organization brings to its product/service. Firms typically provide either growth or margin. Occasionally, a gangster appears and offers both. Peloton is not Facebook or Google, but it has greater margins than Apple and (law of smaller numbers) is growing much faster than the Four, 77% YOY.

Accelerant: Peloton attracts premier talent from top fitness studios to exclusively teach within the Peloton ecosystem. These instructors are poached from the likes of SoulCycle, Equinox, and Barry’s Bootcamp. Peloton pays instructors $500 per class (over three times that offered by SoulCycle and nine times Equinox) and awards instructors equity in the business, giving them a vested interest in the firm’s growth. In turn, instructors achieve celebrity status, some building social audiences well over 300,000.

Vertical — hardware: 85% of Peloton’s connected subscribers own Peloton-manufactured equipment, enabling control over the experience and differentiation.

Vertical — fulfillment: Peloton also fulfills 58% of its orders (delivery and setup). This vertical integration allows the company to create a customer-centric experience and earn a net promoter score of 86. This is off the charts. The firm frequently mentions its goal to be the first 100 NPS company.

Appleton (rundle and flywheel)

The only thing better than recurring revenue is a recurring revenue bundle that could form a flywheel. Peloton riders are fanatics. There are over 250,000 members of the wildly popular Official Peloton Member Facebook page. These people post 23 times per hour and interact with each other through comments and likes. Just as The League introduces Ivy League socialites to each other (shouldn’t it be called “Douche-League?”), JDate connects Jewish singles, and Raya connects models and the social elite, Peloton could begin connecting fitness-minded singles who become more engaged, riding, and swiping.

I believe there is a floor on the stock as there are few firms that are a more obvious/natural acquisition by Apple than Peloton. Apple could pay a 50% premium for all the outstanding stock of the Apple of fitness and register less than a 1% dilution. The acquisition of Peloton would provide the world’s most valuable firm with an additional, if more cumbersome, wearable that has greater margins than the most profitable product in history, the iPhone. The tie-up would also take Apple from letter D to G in one of only two sectors that can move the needle on a $1.3 trillion firm — health care. (The other is education.)

The stock is now a broken IPO, trading below its initial offering, but the business will likely grow into or past its rationalized value. Unlike the rest of the economy, Peloton has wind in its pedals.

Life is risks

Nothing wonderful happens without taking an uncomfortable risk. I’ll be dead soon, regardless — it’s all going so damn fast. Every night I put my sons to bed, I ask a nonexistent god where the pause button is. So, over the next few weeks, I plan to go to meetings, travel by plane, and shake any hand extended. I’ll have some price-gouged Purell in my back pocket.

Life is so rich,

Scott

P.S. My new podcast, The Prof G Show, launches in two weeks. Subscribe on Spotify, Apple, or anywhere else you get your podcasts.

Originally published on profgalloway.com.